What Happened

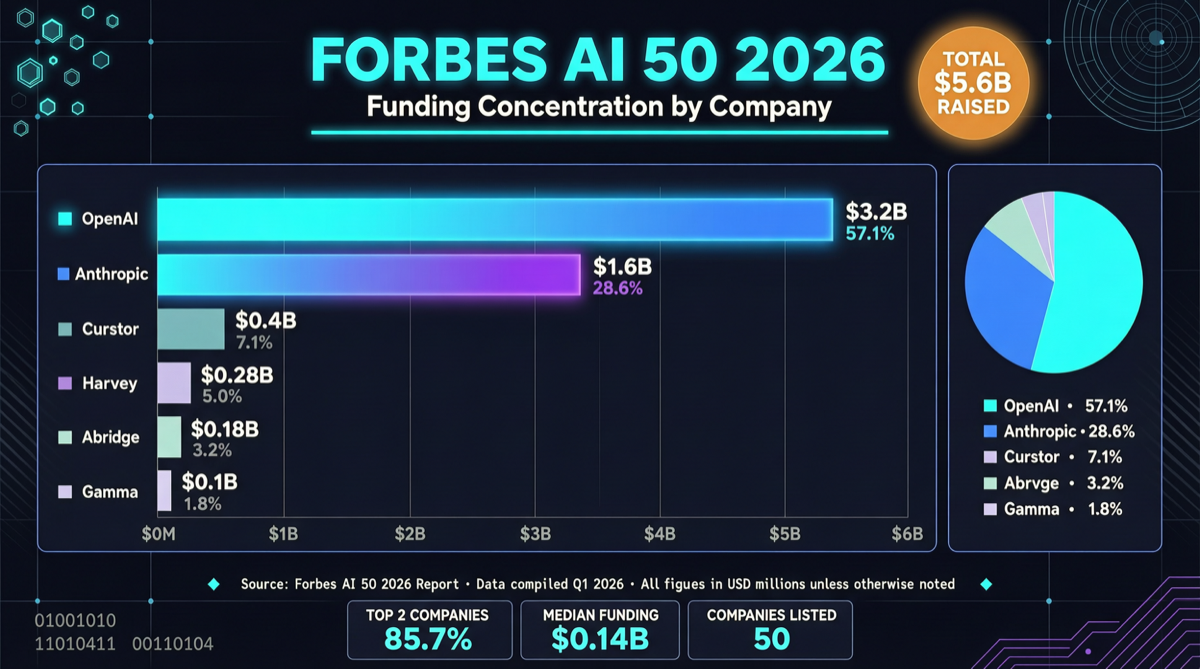

Forbes released its 2026 AI 50 list, with the 50 selected companies holding a combined funding total of $305.6 billion. Of this, OpenAI and Anthropic alone account for approximately 80% of the share.

On the surface, this looks like “model layer monopoly,” but a closer look at the list structure reveals a more important signal.

Layer Breakdown

Top Tier: The Capital Black Hole of Model Giants

| Company | Valuation/Funding | Positioning |

|---|---|---|

| OpenAI | ~$300B+ | General AGI, ChatGPT + Codex + GPT-5.5 |

| Anthropic | ~$180B+ | Safety-first Claude series, enterprise AI services |

Combined, these two companies have raised over $240 billion. This is no longer a “sector” — it’s a gravitational center that has absorbed the vast majority of capital across the entire AI industry.

Next Tier: Vertical AI Apps Prove Commercial Viability

What’s worth paying attention to isn’t the top — it’s the second tier right below it. These companies prove that AI isn’t just about burning money; it can generate revenue:

| Company | Key Data | Vertical |

|---|---|---|

| Cursor | $29B valuation | AI coding tool |

| Harvey | Not disclosed | Legal AI operations |

| Abridge | Not disclosed | Clinical AI |

| Gamma | $100M ARR, 500K+ users | AI presentation/document generation |

Gamma is particularly noteworthy — $100M ARR means it has successfully navigated the path from AI tool to sustainable revenue.

Why This Data Matters

Three judgments:

1. Capital is shifting from “betting on models” to “betting on applications” After $240 billion bet on foundational models, the flow of the next $60 billion is where investors are really voting. The existence of Cursor, Gamma, Harvey, and others shows that: the commercialization window for AI applications has opened.

2. Developer tools are the first vertical to crack commercial viability Cursor’s $29B valuation far exceeds most traditional SaaS companies. Behind this is the real willingness to pay for AI coding tools — developers are willing to pay for tools that 2-3x their productivity.

3. The absence of Chinese AI companies is a structural problem Almost no Chinese companies appear on the Forbes AI 50 list. This isn’t because Chinese AI companies aren’t strong enough (DeepSeek, Kimi, Qwen have caught up technologically) — it’s the combined effect of funding structure, IPO paths, and geopolitical factors.

Investment Logic

If you’re looking for investment opportunities in the AI sector, this list signals:

- Short term: Focus on vertical AI apps that have cracked ARR (Gamma model)

- Medium term: AI coding tools (Cursor model) still have room to grow, but competition is intensifying

- Long term: The winners in foundational models are largely determined (OpenAI, Anthropic, Google). New entrants need differentiation

Bottom line: 80% of $305.6B concentrated in two companies — that’s not a healthy industry structure. But the Cursor and Gamma tier below are proving that AI’s business model isn’t just “burn money to build models.”