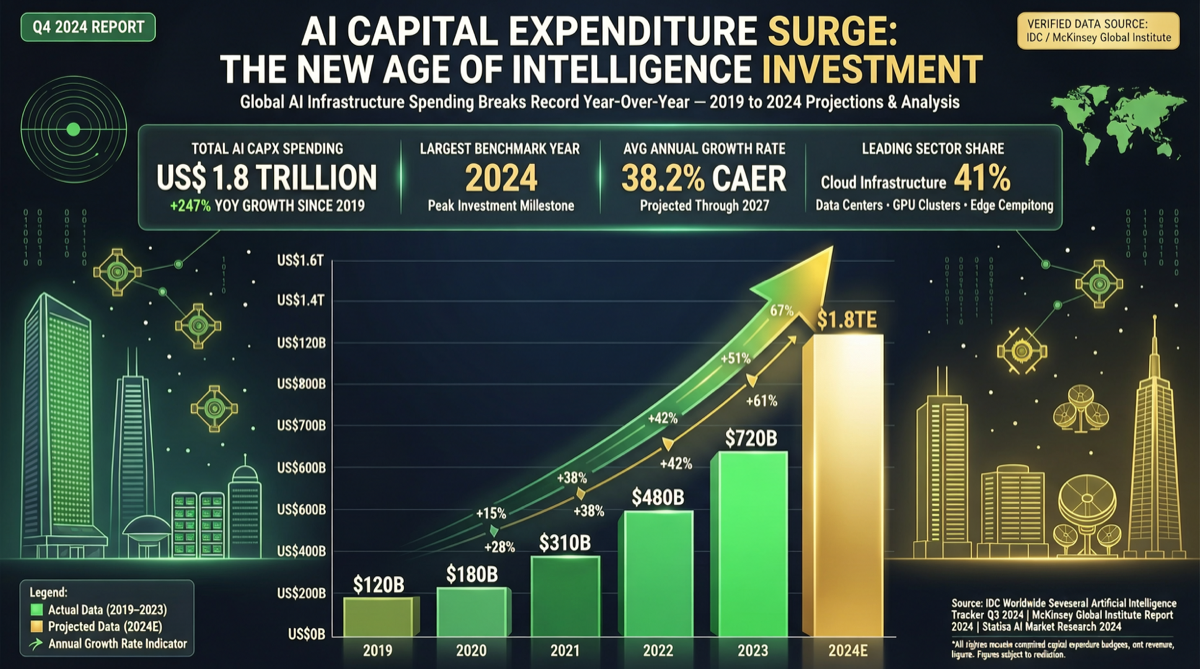

Key Data

| Company | Q1 Cloud/AI Revenue Growth | 2026 CapEx Guidance | Change |

|---|---|---|---|

| Google (Alphabet) | Cloud +63% | $180-190B | Up $5-10B |

| Meta | - | $125-145B | Up $10B |

| AWS (Amazon) | +28% (fastest in 15 quarters) | Not separately disclosed | Significant acceleration |

| Azure (Microsoft) | +40% | Not separately disclosed | Cloud growth driver |

Meta: Another $10B Added

Meta raised its 2026 CapEx guidance to $125-145B, an increase of $10B. Zuckerberg stated:

“AI is the infrastructure of the next decade, and our investment in compute will directly determine our competitive position.”

Google: 63% Cloud Growth, Supply Chain Bottleneck

Google’s cloud revenue grew 63%, but Sundar Pichai admitted supply remains constrained. This means demand far exceeds supply — Google is fighting for chips, racks, and power.

What This Means

1. From “Model Race” to “Compute Race”

The competition has shifted from “whose model is better” to “who has more compute.”

2. Chip Supply Chain Remains Tight

Google publicly acknowledging supply constraints means NVIDIA GPUs remain in high demand, and custom chips (TPU, MTIA, Trainium) become increasingly important.

3. Small Players Get Squeezed

When Big Four AI CapEx approaches $500B+ in 2026 alone, smaller AI companies face insurmountable cost, talent, data, and distribution gaps.

Investment Logic

| Beneficiary | Examples | Logic |

|---|---|---|

| GPU chips | NVIDIA, AMD | Selling the pickaxes |

| Chip design IP | ARM, Broadcom | Big tech needs IP for custom chips |

| Data center REITs | Real estate | Compute needs physical space |

| Power/energy | Nuclear, renewables | AI is power-hungry |

Summary

The Q1 earnings send a clear signal: AI infrastructure investment is structural acceleration, not cyclical fluctuation.

When Meta is willing to spend a mid-sized country’s GDP on AI, the rules of the game have changed.