What Happened

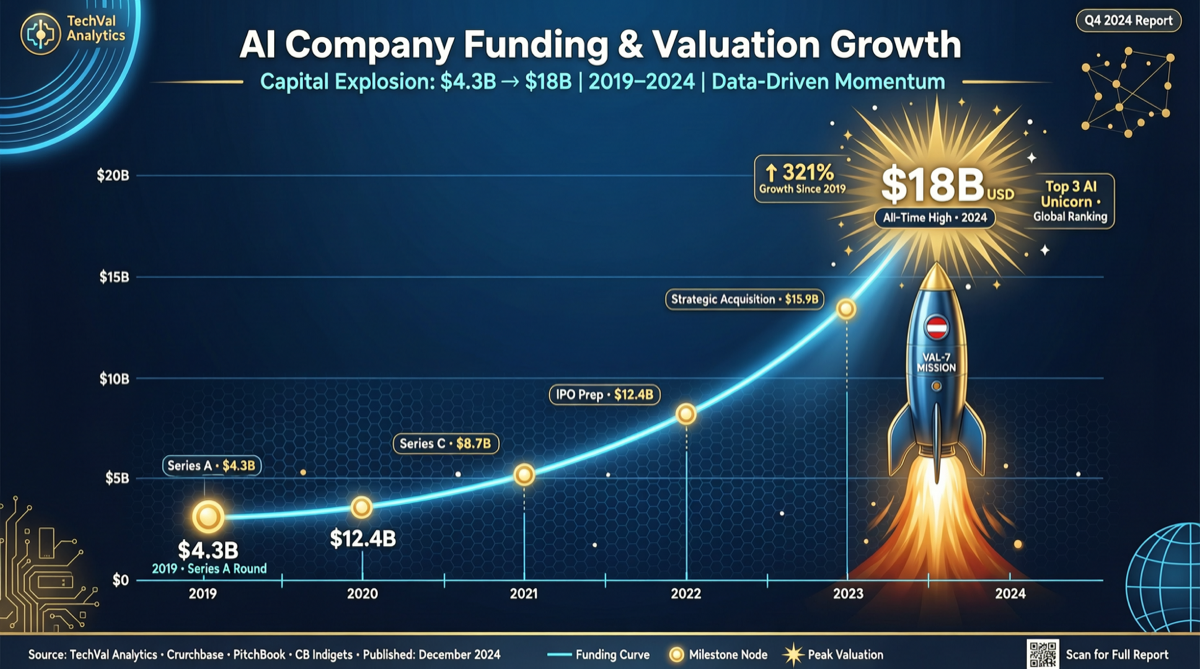

Moonshot AI (Moonshot AI, parent company of Kimi) is accumulating capital at a staggering pace. Cross-verified by multiple sources:

| Round | Date | Amount | Valuation |

|---|---|---|---|

| Series A | Late 2025 | $500M | $4.3B |

| Series B | Feb 2026 | $700M | $10B |

| Series C | Mar 2026 | $1B | $18B |

In less than 90 days, the valuation multiplied over 4x. This is nearly unprecedented in the history of Chinese AI startups.

Product Roadmap Meets Capital Momentum

Behind the valuation surge lies Moonshot AI’s aggressive product roadmap:

- Kimi K2.6: Scheduled for June 2026 launch, reportedly with major breakthroughs in coding and long-context understanding

- Kimi K3: Already in intensive internal testing, total parameters exceed 2.5 trillion, with experiments running well beyond 1 million token context

- Kimi Claw: Moonshot AI’s Agent product, already listed among competitors in the “Hundred Shrimp War” alongside Tencent and others

Capital markets are sending a clear signal: Moonshot AI is transforming from “a rising star with long-context capabilities” to “a full-stack AGI platform.”

Valuation Logic Breakdown

What does an $18B valuation mean? Horizontal comparison:

| Company | Valuation/Market Cap | Key Metrics |

|---|---|---|

| OpenAI | ~$300B | GPT-5.5, ChatGPT 400M users |

| Anthropic | ~$200B | Claude Opus 4.7, $10B annual revenue |

| Moonshot AI | $18B | Kimi DAU growing rapidly, K3 in development |

Moonshot AI’s valuation stands at roughly 9% of Anthropic’s. If Kimi K3 can reach 80% of GPT-5.5/Claude Opus 4.7’s coding capabilities, this valuation is not exaggerated.

Risk Signals

- Compute bottleneck: Training a 2.5 trillion parameter model requires massive advanced GPUs, while US export controls continue to tighten

- Commercialization pressure: An $18B valuation demands matching revenue growth, but Kimi’s paid conversion rate remains an industry secret

- Competition heating up: Zhipu GLM 5.1, DeepSeek V4 Pro, and Qwen 3.6 are all advancing simultaneously

Actionable Advice

- Developers: Watch Kimi K2.6’s API pricing strategy. If the price-performance ratio beats GPT-5.5, consider it as a primary model backup

- Investors: The $18B valuation has already priced in massive optimism; short-term correction risk cannot be ignored

- Enterprise users: Moonshot AI’s funding speed means service stability is assured, but note that its product line is still rapidly iterating